Labuan Co Basis Period

A For Non-Trading Company investment holding zero tax and no audit report. View L8 Labuan companypdf from TAX BBFT3013 at Tunku Abdul Rahman University College Kuala Lumpur.

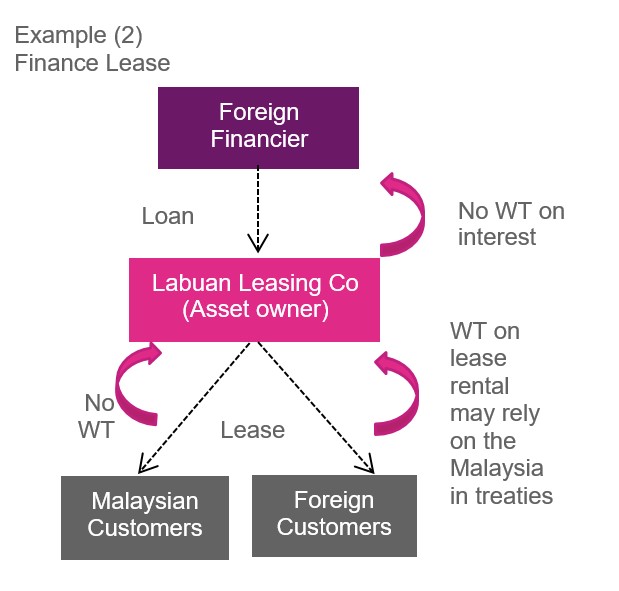

Labuan Leasing Business Jtc Kensington

All income of persons other than a company.

Labuan co basis period. Guidelines on Valuation Basis for Liabilities of Labuan Life Insurance Business. A Labuan entity carrying on a Labuan trading activity for the basis period for a YA can enjoy the preferential tax rate of 3 of its audited net profits or elect to pay tax of RM20000 for a YA. B For Trading Company will be taxed at a rate of 3 on net audited profits.

D All Labuan companies can opt to have a Permanent Election to be taxed. The basis period for a company co-operative or trust body is normally the financial year FY ending in that particular YA. The Regulations which were gazetted on 31 December 2018 and.

Ii If the basis period for a YA the surrendering company first commences operation is less or more than 12 months the surrendering company is commence surrendering its adjusted losses immediately after the second basis period. Guidelines on the Conduct and Roles of Labuan Insurance and Takaful Brokers. For example the basis period for the YA 2018 for a company which closes its accounts on 30 June 2018 is the FY ending 30 June 2018.

Dormant or inactive Labuan Company are required to submit relevant tax documents on an annual basis until the company is officially struck off or removed from the Labuan Register. C For Dormant Company zero tax and no audit report. Introduction of provisions for the creation of treasury shares and.

Allow a Labuan company to issue shares which may be divided into one or more classes and also to issue fractions of its shares. If a Labuan entity does not fulfil the minimum operating expenditure or employment requirements specified in the Principal Regulations for a basis period for a year of assessment it will be subject to tax at the rate of 24 of its chargeable profits for that year of assessment under the Act. Generally due to the nature of the company management accounts will suffice with no tax and audit report required.

Basis period for a year of assessment means the accounting period or periods ending in the preceding calendar year. 1 Section 3A states that a Labuan entity carrying on a Labuan business activity may make an irrevocable election in the prescribed form so that any profit of the Labuan entity for any basis period for a year of assessment and subsequent basis periods to be charged to tax rate in. Income derived from a Labuan non-trading activity for the basis period for a YA is exempt from tax for that year of assessment.

The pronouncement made by LFSA earlier that any Labuan entity carrying on a Labuan business activity but fails to comply with the relevant substance requirements for a basis period for a year of assessment is subject to tax under the LBATA at the rate of 24 of its chargeable. Labuan Companies Act 1990 Removal of the requirement to obtain approval for dealings between Malaysian residents and Labuan companies. For example year of assessment 2020 for a Labuan entity having an accounting period ending 31 December refers to its accounting period ending 31 December 2019.

Guidelines on Investment Management for Labuan Insurance and Takaful Business. If a Labuan entity does not fulfil the minimum operating expenditure or employment requirements specified in the Principal Regulations for a basis period for a year of assessment it will be subject to tax at the rate of 24 of its chargeable profits for that year of assessment under the Act. 1846Labuan was ceded to Britain and made a Crown colony.

1963Labuan became a part of Sabah in independent Malaysia. Lesson 8 Labuan Company Labuan business activities Labuan trading activity Labuan. A tax rebate is granted to a Labuan company for each year of assessment for any business zakat which is paid in the basis period for that year of assessment to and evidenced by a receipt issued by a Labuan Islamic religious authority.

Consists of a basis period of 12 months the company first commences operation. Business Activity Tax Requirements for Labuan Business Activity Regulations 2018 PUA 3922018 for a basis period for a year of assessment YA shall be taxed at the rate of 24 upon its chargeable profits for that YA under the Labuan Business Activity Tax Act 1990 the LBATA. Guidelines on Valuation Basis for Liabilities of Labuan Family Takaful Business.

The most appealing feature of the Labuan tax regime is the attractive tax of 3 per cent on net audited profits provided substance requirements prescribed minimum headcount and operational expenditure in Labuan are met throughout the relevant basis period. 1990On 1 October 1990 Labuan was declared an International Financial Centre. Four 4 tax options for Labuan Company are as follow.

1984Labuan was declared a Federal Territory.

Komentar

Posting Komentar